Date:2022-08-26 10:46:20 Views:969

There are several indications that the shortage of semiconductors for automotive applications has eased. However, light-vehicle production is likely to remain below expectations through at least 2023.

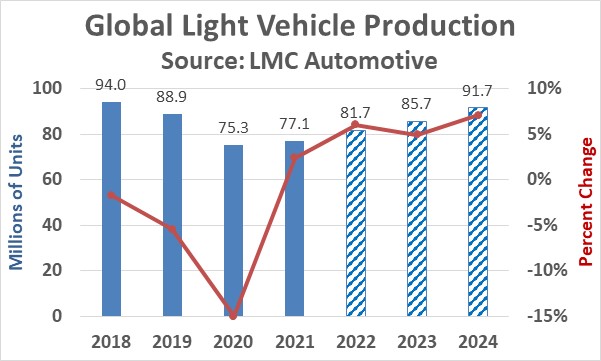

LMC Automotive's July forecast for light vehicle production is 81.7 million units in 2022, up 2 percent from 2021. The LMC's April forecast for 2023 and 2024 is 4 million units per year higher than the July forecast. Production of 91.7 million units by 2024 should still be below the pre-pandemic level of 94 million units five years ago in 2018.

The main reason for the oversupply of automotive semiconductors is that

Automakers severely cut semiconductor orders at the start of the COVID-19 pandemic in early 2020. If demand drops significantly as a result of the pandemic, auto companies fear they will be stuck with an overstock of vehicles. As automakers try to increase orders, they lose ground in the queue, falling behind other industries such as personal computers and smartphones.

Many automakers use just-in-time ordering systems to avoid inventory overhang. This leaves them with little to no buffer inventory. In addition, most semiconductors used in automobiles are purchased by the companies that supply the systems (engine controls, dashboard electronics, etc.) rather than the automaker, which leads to a more complex supply chain.

The semiconductors used in automobiles have long design cycles and must be of a qualified standard. As a result, it is difficult for automakers to change suppliers in a short period of time.

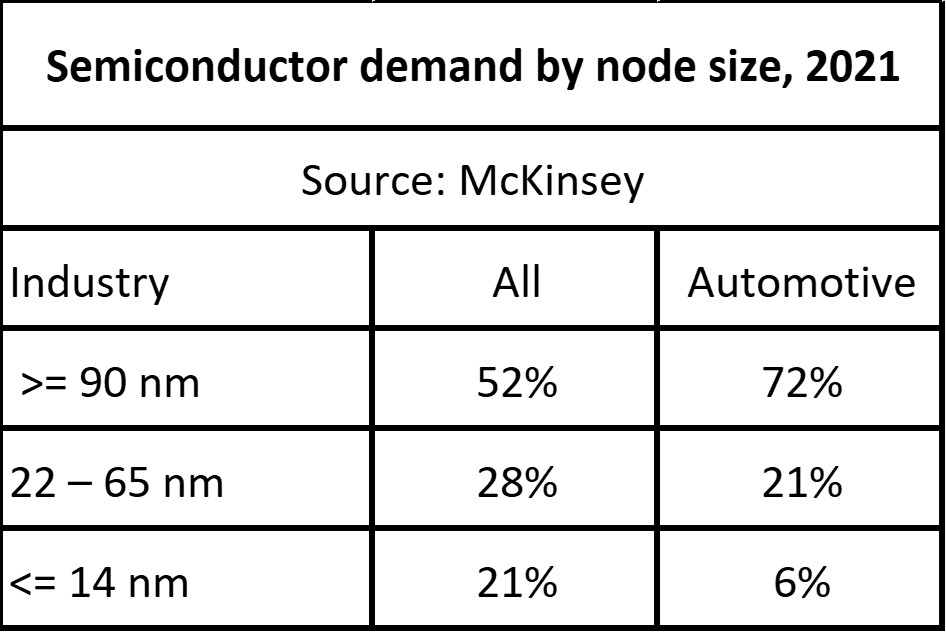

Because of the long design cycles and product lifetimes, semiconductors used in automotive applications use older process nodes than most other applications. As shown in the table below, McKinsey estimates that 72% of automotive semiconductor wafers will use 90nm or more mature process nodes by 2021, compared to 52% of all applications. Only 6% of automotive demand is for 14nm and less process nodes, compared to 21% across all applications. Semiconductor manufacturers are focusing their capital expenditures on more advanced process nodes, with only modest capacity expansion at older nodes. TSMC, the dominant foundry, derives 65% of its revenue from advanced process nodes, with only 12% of revenue coming from 90nm or larger nodes. Only 5% of TSMC's revenue comes from automotive, compared to 38% from smartphones.

Given all of the above factors, it will take time to resolve all supply issues. Recent comments from major automakers reveal a mixed trend in addressing the semiconductor shortage.

Toyota - shortage will not occur until at least the third quarter of 2022

Volkswagen - shortage alleviated

Hyundai - shortage alleviated

GM - shortage impact through 2023

Stellantis - shortage through H2 2022

Honda - Uncertain outlook due to shortage

Nissan - recovery in coming months

Ford - shortage still an issue

Mercedes-Benz - no major supply issues

BMW - no production delays due to shortages

Volvo - recovery of adequate supply

Bosch (parts supplier) - shortage until 2023

The five largest automotive semiconductor suppliers also took a different view of the shortage outlook in their most recent Q2 2022 financial reports.

Infineon Technologies - shortage to ease gradually in 2022

NXP Semiconductors - demand to continue to outpace supply in Q3 2022

Renesas Electronics - Inventories to return to planned levels by the end of Q2 2022

Texas Instruments - inventories still below expected levels

STMicroelectronics - capacity sold out by 2023

The shortage of automotive semiconductors is likely to continue at least through 2023. While some automakers say they have returned to full production, most report that the shortage continues. The shortage will prevent automakers from producing enough cars to meet demand in 2022 and 2023, resulting in continued high prices for most cars.

Automakers and semiconductor suppliers are working to prevent such severe shortages in the future. Automakers are adjusting their just-in-time inventory models. Automakers are also working more closely with semiconductor suppliers to communicate their short- and long-term needs. As the trend toward electric vehicles and driver assistance technology continues, semiconductors will become even more important to automakers.

Phone:+86-137-5112-7429

Email:sales@hyx-tech.com

Address:14D2, block A, Modern window building,ZhenHua Road,Futian District, Shenzhen

sales@hyx-tech.com

sales@hyx-tech.com +86-0755-2399-7487

+86-0755-2399-7487 sales@hyx-tech.com

sales@hyx-tech.com Login

Login Register

Register