Date:2022-07-20 14:18:19 Views:964

How hot the chip last year, how frightening this year.

There is no doubt that the current development of the entire chip industry has shown a fire and ice. On the one hand, part of the chip shortage is still ongoing, the major chip makers expansion and capital expenditure is also in stride, showing a red-hot situation; while on the other hand revealed that the beginning of the year has been a wild fall in the share prices of the giant so far, and began to shake down the price of chips.

From driver chips, analog chips, to consumer MCUs, storage chips, GPUs, no matter how "hard to find a core", it seems that now all can not escape the fate of price reductions.

The first to bear the brunt of the driver chip

Data shows that the price of driver chips has fallen by about 40%.

In the 2020 epidemic stimulated by the "home economy" to drive people to work at home, study, entertainment and other applications of demand, the display industry has also achieved rapid development, the upstream display driver chip simultaneous booming. omdia data show that in 2020, the total demand for display driver chips is double-digit growth, amounting to 8.07 In 2021, the growth of IT applications remains strong, while the total demand is expected to grow to 8.4 billion due to the increase in penetration of higher resolution in TV panels.

The hot market makes drive chip companies, especially Taiwan-based drive chip manufacturers become big winners. In TrendForce Tibco announced the world's top 10 IC design companies in 2021, Taiwan enterprises Lian Wing, Rui Yu, Qi Jing Optoelectronics three rankings have improved, including Lian Wing and Qi Jing Optoelectronics 2021 revenue growth of up to 79%, 74%, ranked first and second, Qi Jing

Optoelectronics also replaced Dai Leger, successfully squeezed into the top ten seats.

However, the tide comes and goes quickly.

Under the influence of factors such as high inflation and cooling of the house economy, TV, Notebook and Monitor market demand is facing contraction, TV majors are cutting their orders and TV panels are cutting their prices. According to TheElec, Samsung has suspended the purchase of LCD panels from its suppliers until further notice. Not only Samsung Electronics, but also top TV makers including LG

Electronics, China's TCL and Japan's Sony are all reducing their annual TV shipment plans this year.

The market downturn, coupled with the easing of the contradiction between supply and demand in the driver chip market, so that the panel driver IC factory hit the chip cut single first shot, the industry rumors at the end of May, certain driver IC factory big cut foundry capacity, the range of up to 20%-30%.

And from the major drive IC factory's latest financial report, we can also see that the drive IC factory scenery has become a big profit in the past.

On July 6, the United Wing announced June consolidated revenue of 8.158 billion NTD, a monthly decline of 25.7%, not only fell below the 10 billion NTD barrier, but also wrote a new low since February 2021, and the second quarter revenue of only 31.461 billion NTD, a quarterly decline of 13.8%, significantly lower than the second quarter revenue of 34.5-35.8 billion NTD, a new low since five quarters.

On June 21, Chiken Photoelectric announced its forecast for the second quarter results ending June 30, 2022. According to the report, Chiken's operating income is expected to decline 22%-27% sequentially, compared to the previous forecast that it would decline 16%-20% sequentially.

Mr. Jordan Wu, President and Chief Executive Officer of Chipset, said, "The revised second quarter earnings report forecast reflects a weaker macro environment and slower end market demand, which is a result of recent interest rate increases and inflationary pressures. In response, we are cutting production and further tightening inventory levels.

In terms of mainland manufacturers, Fu Man Micro, Ming Microelectronics and Jingfeng Mingyuan, three manufacturers involved in the LED driver chip business, have already experienced a significant ringgit decline in net profit as early as the fourth quarter of 2021, perhaps from that time, the first signs of price cuts have already appeared.

Local manufacturers are poised to launch the analog chip

In addition to the driver chip, all signs also indicate that the overall situation of the analog chip market is also in sharp decline. In early June this year, the supply chain news that the global analog IC leader TI informed customers that the imbalance between supply and demand in the second half of the year will ease. Some industry insiders even said that TI chips fell by more than 80%. Although TI said the rumors are not true, but the power management chip led by the analog IC price carnival ended, and even face the pressure of falling prices is a reality that has to face.

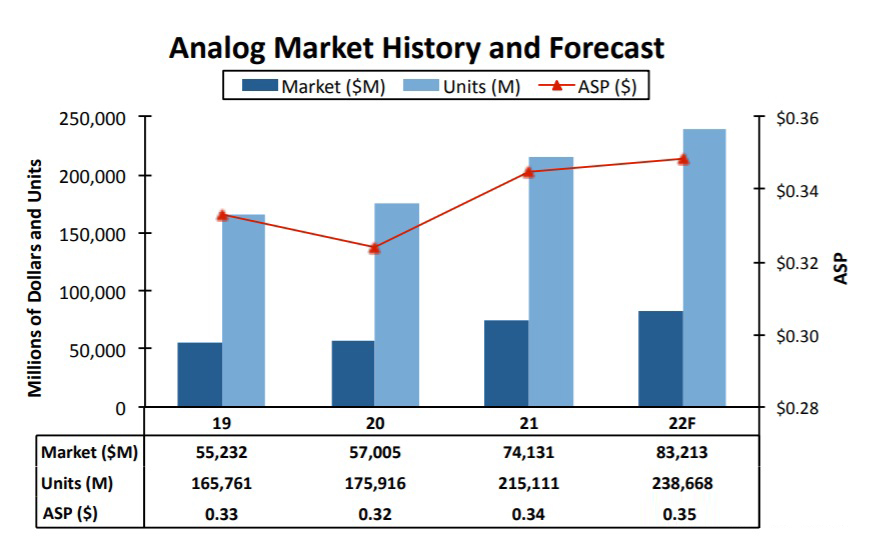

Last year by the epidemic, the impact of natural disasters, coupled with new energy vehicles, 5G and other emerging areas of strong demand, the analog chip market ushered in a period of high before all. IC Insights data show that the analog market in 2021 with a stunning 30% growth in sales to a record high of $ 74.1 billion, shipments also climbed 22% year-on-year to 2151 A record level of 100 million units in size.

In addition to record market sales, the average sales price of analog chips also rose by 6% last year, which is understood to be the average price of analog ICs after a long absence of 17 years (since 2004) again doubled. From the previous first securities statistics of the U.S. stock market value of more than $ 10 billion semiconductor companies 2021 gross margin can be found, five analog chip makers gross margin of more than 50%, including Texas Instruments is to take the top of the list, gross margin of 67.5%, and its gross margin in the first quarter of this year was raised to 70.2%.

The hot market makes a number of analog chip makers began to expand production and investment in a big way. However, by this year, with the rapid opening of new production capacity and downstream demand began to sluggish, the problem of tight analog chip capacity has been significantly alleviated, the chip prices naturally fell.

Some industry insiders said that Texas Instruments TPS61021ADSGR this power management chip, in May 2021 rose to a maximum price of $ 45 per unit, has now dropped to "five or six dollars" per unit.

In May this year, Texas Instruments Chief Financial Officer Rafael Lizard said that the impact of the epidemic in the mainland, the second quarter revenue estimates will be revised down by 10%. However, even though the revenue forecast was revised down, Texas Instruments' expansion continues, and it announced on May 19 that it broke ground on a new 12-inch semiconductor wafer manufacturing site in Sherman,

Texas, with plans to build four factories to meet long-term market demand.

In terms of local analog chips, benefiting from last year's continued strong market demand, the overall local analog chip manufacturers to achieve faster growth in 2021, and in the recent past, including micro-source shares, South Core Technology, MeiXinSheng, TuoEr micro, JieHuaTe, YuTai shares, NanLin Electronics, DiO Micro, etc., a number of analog chip companies have opened the road to listing.

However, in the face of the end of the carnival, the future of analog chip local manufacturers are still challenging.

MCU: automotive, industrial control category "good", the Consumer category "crying"

The MCU market has also been thriving in the past 2021, with a serious imbalance between supply and demand and the consequent price hikes, with individual popular models rising up to more than 10 times. IC Insights reports that the global MCU market grew by a whopping 27% in 2021, which is the highest growth rate since the 21st century.

However, it should be noted that the price drop is only part of the consumer MCU, automotive, industrial control and other applications of MCU demand is still very strong, so the price is also relatively stable. What's more, industry insiders say that this consumer MCU price drop is mainly caused by IC distributors rather than chip makers to expand production.

Since this year, with many chip makers in the cell phone and PC supply chain cut orders, the upstream foundry capacity gradually released, the original shortage of MCU to get more capacity support. Data shows that in March this year, the general MCU delivery time has started to return to the normal level of 8-12 weeks.

However, at that time, MCU vendors and some channels and customers stocked up based on the unstable international form, and inventory could last three to four months, making the supply and demand relationship failed to be eased. So much so that, to this day, IC distributors have had to start lowering the prices of consumer-grade MCUs in response to this year's sluggish market.

In terms of application areas, this price reduction may have a greater impact on Chinese and Taiwanese manufacturers than on foreign MCU makers. In terms of global MCU downstream applications, automotive accounts for 39%, industrial control accounts for 27%, and consumer accounts for 18%, but in the downstream applications of MCU in China, the consumer field ranks first, accounting for 27%, while the automotive and industrial control fields, which are the main focus of foreign majors, have formed a serious supply-demand gap with the dramatic increase in downstream demand and the lack of output from upstream enterprises, and the prices are still very substantial.

In the face of declining prices, a spokesman for Holtek Semiconductor in Taiwan, China, said at the end of April that consumer MCU pricing in the mainland market was confusing and that the company would let its distribution partners make price adjustments.

In addition, another MCU maker, Nuvoton Technology, also performed relatively flat in April and May this year, with revenue down 2.18% and 3.04% YoY, and up 6.04% and 6.61% YoY respectively, losing the scenery of last year's profit surge of more than 5.5 times and net earnings per share of NTD7.27.

On the mainland, domestic MCU players such as Zhaoyi Innovation, Zhongying Electronics and SMIC have gradually started to shift from home appliances and consumer electronics to automotive and other fields.

Zhaoyi Innovation's first automotive-grade MCU product was flowed in March and entered the customer sample testing stage, and is expected to achieve mass production around mid-2022; Zhongying Electronics is mainly used for the body control MCU part, and is expected to flow back in the middle of the year; Zhongmicro Semiconductor has shown its determination to develop automotive-grade chips in its prospectus, and its IPO plans to raise 729 million yuan, with 283 million yuan to be used for automotive-grade chips R&D projects.

Memory chips: a new round of market reshuffle or inevitable

Affected by the demand for consumer electronics in China's closed cities, coupled with the uncertainty of the general environment, memory chips have also begun to reduce prices. Among them, low-capacity NOR flash memory is expected to drop by around 3%, and TrendForce data shows that the average contract price of DRAM fell 10.6% year-on-year in the second quarter of this year, the first drop in 2 years, while NAND prices continue to fluctuate.

What's more, sources point out that in the spot market, memory prices have been falling rapidly since the second quarter, with almost all types of memory prices set to fall by more than 10 percent sequentially in the third quarter of 2022. Tiburon Consulting also predicts that the average contract price for DRAM will fall 21 percent sequentially in the third quarter, while NAND's sequential price drop is at 12 percent.

Memory chips also had a period of high light. 2020, the international storage chip majors occurred in a variety of accidents such as fires, power outages, floods, etc., became an important driver of the rise in storage chip prices. wind statistics show that the NAND Flash market prices in the first half of last year to maintain the upward trend, although the second half of last year in the drop in price range, but by the first half of this year Western data and armor man part of the NAND production line was contaminated, resulting in a quarter of capacity damage, the major storage manufacturers have started a new round of price increases wave.

However, under the impact of hyperinflation and the downturn in the consumer market, not only the traditional consumer electronics sector, cloud and server storage chip sales also began to be affected, companies continue to cut back on support, resulting in server downstream customers worried about possible inventory impairment losses under the price reduction cycle, and therefore delayed the purchase of server memory.

Storage major Micron's pessimistic expectations seem to be more evidence of the current storage market turmoil. Micron Technology warned that the company's revenue for the fourth quarter of fiscal 2022 is expected to be around $7.2 billion, well below analysts' expectations of $9.14 billion, amid negative impacts such as weak demand for consumer electronics (mainly PCs and smartphones) due to the Russia-Ukraine conflict and high inflation.

Sanjay Mehrotra, Micron's chief executive officer, said that weak consumer market end demand, including personal computers (PCs) and smartphones, is significantly dragging down global memory industry demand. Despite strong data center end demand, Micron has seen some customers intend to cut their memory and storage inventories.

In addition to Micron, Samsung, for its part, has suspended purchases from all business units including panels, cell phones and memory chips. More recently, Taiwan's Electronic Times reported that Korean memory makers, including Samsung, will voluntarily cut prices by more than 5 percent in exchange for sales. The market fears that this strategy of price for volume may trigger a value war for the entire industry, and a new round of market reshuffling may be inevitable.

SK Hynix, for its part, said that China's smartphone market demand will continue to be weak, PC shipments due to the new crown anti-epidemic blockade impact production and a slight decline, but consumer PC demand is weak at the same time, corporate, game computer sales will show a solid.

Not afraid to drop the price of the GPU?

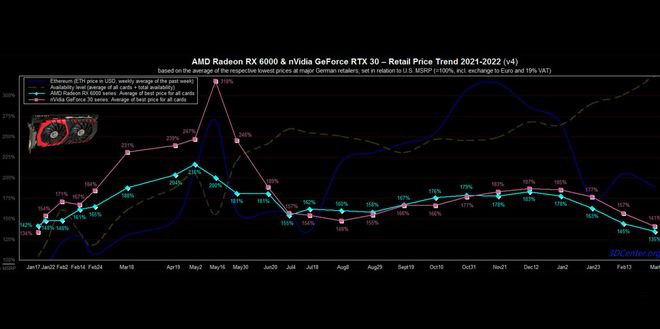

GPUs were also hot last year, as seen in the previously released article "The Golden Age of China's Big Chips", which showed that the GPU capital market was hot last year, and in addition to investor interest, the price of GPUs themselves was also rising. By March of this year, GPU prices began to trend downward, and as of May, PC GPU prices were still in a steady downward trend.

The data shows that eBay prices for the best graphics cards (i.e., current-generation hardware) have dropped an average of 14 percent since June 1, and previous-generation cards have dropped an average of 17 percent. As early as March of this year, GPU leader Nvidia had informed downstream graphics card manufacturers that its GPU prices had been reduced by roughly 8% to 12% due to lower costs.

The reason for this, on the one hand, is the fading of the mining tide. Since the end of 2020, bitcoin, ethereum and other virtual currencies are hot, driving the price of mining important tools - GPU all the way up, Nvidia RTX 3080 once rose to more than 16,000 yuan, a card difficult to find phenomenon occurs frequently. However, as virtual currency prices continue to fall, as well as countries around the world to strengthen restrictions on the mining of virtual currency behavior, the merger of Ether upgrade progress is not smooth, and so on, the risk of mining is getting bigger and lower returns, a large number of miners out of the coin circle, graphics card prices back down significantly.

The other side is the increase in production capacity, supply and demand began to ease. Intel released its independent graphics card Alchemist GPU for mobile platforms at the end of March this year, when news showed that the desktop platform version is expected to be launched in the second quarter of 2022 for, and the workstation version will be released in the third quarter of 2022, Intel is expected to ship more than 4 million GPUs for use in independent graphics cards in 2022, including mobile platforms, desktop platform and workstation versions.

On the AMD side, it is also rumored that its AMD Radeon RX 7000 series graphics cards are expected to be released in late October to mid-November this year.

However, although GPU prices have fallen, its market outlook remains objective. The current climb in data volumes has made GPUs increasingly important for hyperscale computers, as they handle critical workloads such as recommendation engines much faster than general-purpose server CPU cores.

Facebook's parent company, Meta, has said it needs to quintuple the number of GPUs in its data centers to help it compete with short-form video apps and the long-standing security problem TikTok.

On the local front, the GPU capital fever seems to remain, with Mu Xi just recently announcing the completion of a RMB 1 billion Pre-B round of funding. In addition, GPU companies such as Zhiying

Microelectronics, Deepstream Micro Intelligence, Core Pupil Semiconductor, and Toner Computing Technology have also all announced the completion of financing in the first half of this year.

Write at the end

From the current development point of view, the chip industry ice and fire situation will continue to exist, the era of semiconductor "all the carnival" has ended, local manufacturers, especially small and medium-sized enterprises, how to do well in this flood, or they will have to face the big test.

Phone:+86-137-5112-7429

Email:sales@hyx-tech.com

Address:14D2, block A, Modern window building,ZhenHua Road,Futian District, Shenzhen

sales@hyx-tech.com

sales@hyx-tech.com +86-0755-2399-7487

+86-0755-2399-7487 sales@hyx-tech.com

sales@hyx-tech.com Login

Login Register

Register